October 2023: Q3 San Francisco Apartment Insider

Hello and happy Tuesday!

I hope you are well as we enter the final quarter of the year! The state of the current market is, well……….. functioning and for apartment owners moving in the right direction. I am still seeing solid demand for apartments; primarily on the north to central part of the City.

One of the biggest challenges to get our apartments full is the return to office situation. San Francisco still trails most all major cities in terms of office workers returning to the office. If employers were more stringent in their push to the workforce, we’d have more (apartment) demand. That being said, downtown is a very different place than it was five years ago.

Let’s take a quick look at two dynamics downtown; available office space and the sale of office buildings. In the third quarter, the office market hit a record-high 33.9% vacancy rate. That equates to nearly 30 million square feet listed for lease or sublease. A lot of pundits called the bottom of this market last year, but they were clearly wrong. The talk in the broker community is that showings of available office space (to prospective tenants) is way up. I am not drinking the Kool-Aid that AI companies will save the City, but a good percentage of the showings are to newly funded AI companies.

Looking at sales of office properties in the downtown area, we are seeing some early 1990-era pricing. Examples of the post-COVID world pricing include:

550 California Street, a 355,000 foot office property recently sold for just over $40M, or $114 per foot. Wells Fargo was the seller. It purchased the building in 2005 for $108M.

350 California Street, a 300,000 office property sold for $61M, or $203 per foot.

There are several downtown office buildings going to market that are valued at less than their mortgages (and or are in default). These buildings include:

995 Market Street, a 91,000 foot office building (which has been mostly vacant since August 2021). The owner, Bridgeton Holdings, is more than 30 days delinquent on the $45M loan. WeWork leased approx. 75% of the building through 2031, but opted to terminate its lease early.

55 New Montgomery Street fell behind on payments on the $62.3M note and the lender (Cross Harbor Capital Partners) recorded a notice of default. The owner, Swift Real Estate Partners, bought the 100,200 foot building in 2018 for $64.25M ($641/psf).

222 Kearny Street. In August, GEM Realty Capital missed a payment on a $23.8M loan on the building (partially leased to WeWork, which is now in danger of bankruptcy).

Not quite downtown, but 1045 Bryant Street is in default. The $12.5M mortgage on the property was transferred to a special servicer in August.

Other buildings on the market or soon to close (both of these are owned by Blackrock):

650 Davis Street. A 294,000 foot, three-building office complex is in contract for approx. $90M (or $306 per foot). This property last sold in 2018 for $245M.

600 Townsend Street. A 216,000 foot building will come to market shortly; the expected asking price is in the $60M range, or $290 per foot.

A lot of downtown brokers are playing up the “huge discounts” on many available buildings. Sadly, I don’t see it that way. The value of the asset is tied to (its) ability to generate cash flow from tenants today. The office market, political and business dynamic are shaping the values; and that value is coming in somewhere between $100 and $300 per foot, depending on the class of the building. This is the downtown world of San Francisco today.

On to the rental market. First, hopefully you remembered San Francisco’s Covid-19 tenant protections expired on Aug. 29. After the statewide Covid-19 eviction moratorium ended in July 2022, the Board of Supervisors passed an ordinance stating San Francisco tenants couldn’t be evicted for owing rent due during certain periods of the pandemic. But for rent due on or after Aug. 29, that’s no longer the case. It’s important to note that it does not mean a tenant is automatically evicted — that can only be decided in court. Consult your attorney if you still have non-paying tenants.

Looking at apartment properties, a buyer has been selected for the huge $940 million mortgage portfolio tied to 2,149 San Francisco apartments controlled by Veritas Investments and its partners. Ballast Investments is poised to take over ownership of 75 apartment buildings and become one of the city’s biggest real estate players. Brookfield Corp, a Canadian investment firm is partnering with Ballast and is expected to provide the financing on the transaction. Brookfield is no stranger to San Francisco; on the mall front, they (Brookfield and its partner Westfield) defaulted on the loan for the San Francisco Centre Mall. They also face a $180 million loan deadline in October for the Stonestown Galleria.

As I mentioned earlier, rents are fairly stable. The weighted average asking rent for an apartment in San Francisco has held at ~$3,600 a month. This is the sixth continuous month (at that number) and is 4% lower than at the same time last year.

The weighted average asking rent in San Francisco is still 12% lower than prior to the pandemic

19% below its 2015-era peak of nearly $4,500 a month

The average asking rent for a one-bedroom in San Francisco inched up to $3,050 a month, which is 1% higher than at the same time last year but still 13% lower than prior to the pandemic and 18% below peak.

The number of apartments listed for rent in San Francisco is now 40% higher than at the same time last year, with nearly 60% more studios and one-bedrooms on the market.

What parts of San Francisco are experiencing a resurgence in rents? The Outer Sunset could even be described as booming, with a 15.7% increase in rents since February 2020, which nets out to a median rent of $2,580 for a one-bedroom. Also, rents in Dogpatch have grown 7.7% year over year. It’s the most expensive place to rent in the city, with a median one-bedroom rent of $3,790. On the north side, Cow Hollow rents are 14.8% higher this year when compared with the same period in 2022.

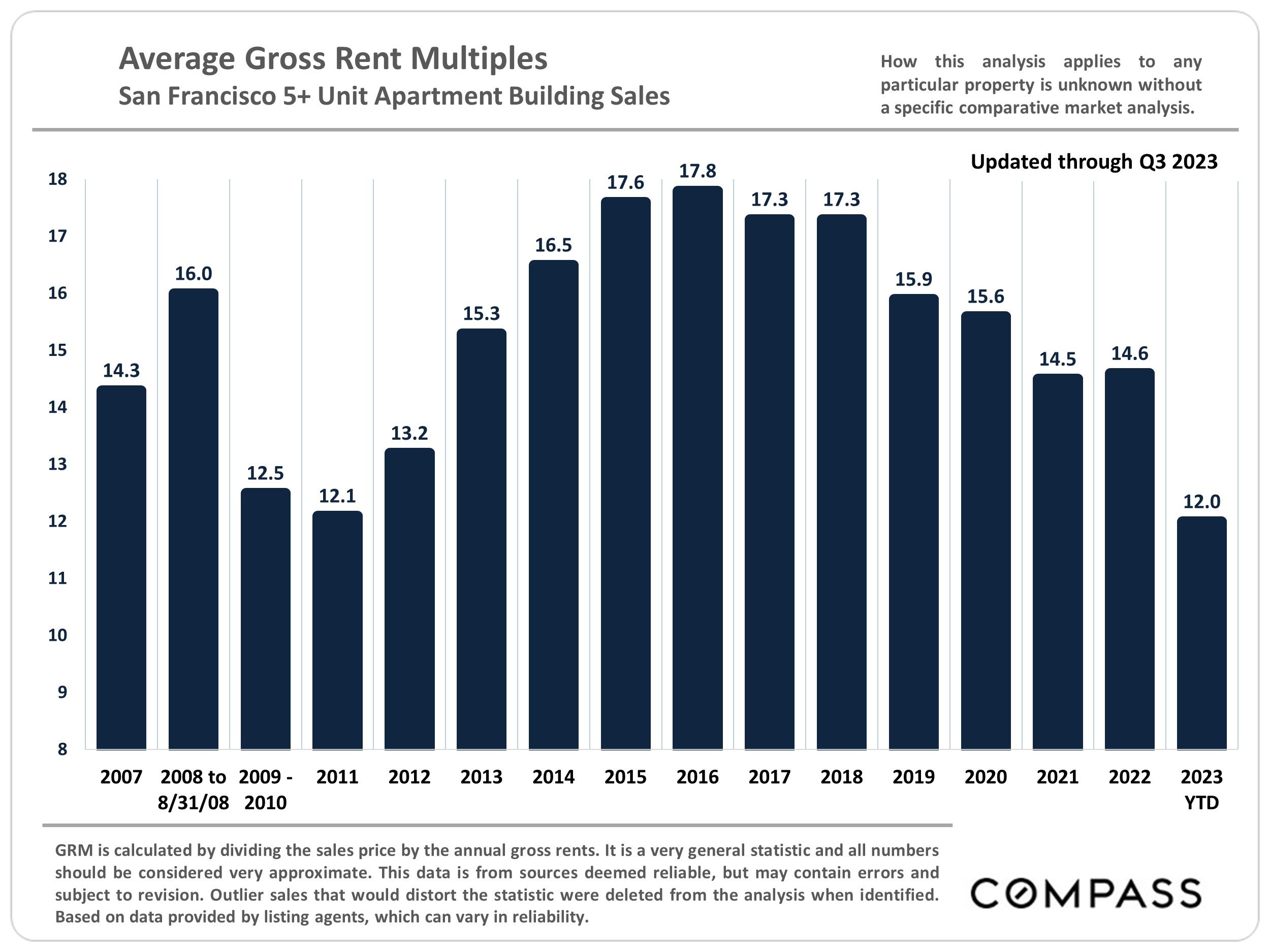

The data points for the quarter: